A top priority subject for anyone within the real estate investing sphere is always taxes, and for good reason – not all investments are created equal when it comes to taxes.

Real Estate investors should be aware that with proper tax strategies in place, they can offset a significant amount of taxes, and free up a great deal of capital, which they can use to further expand their businesses.

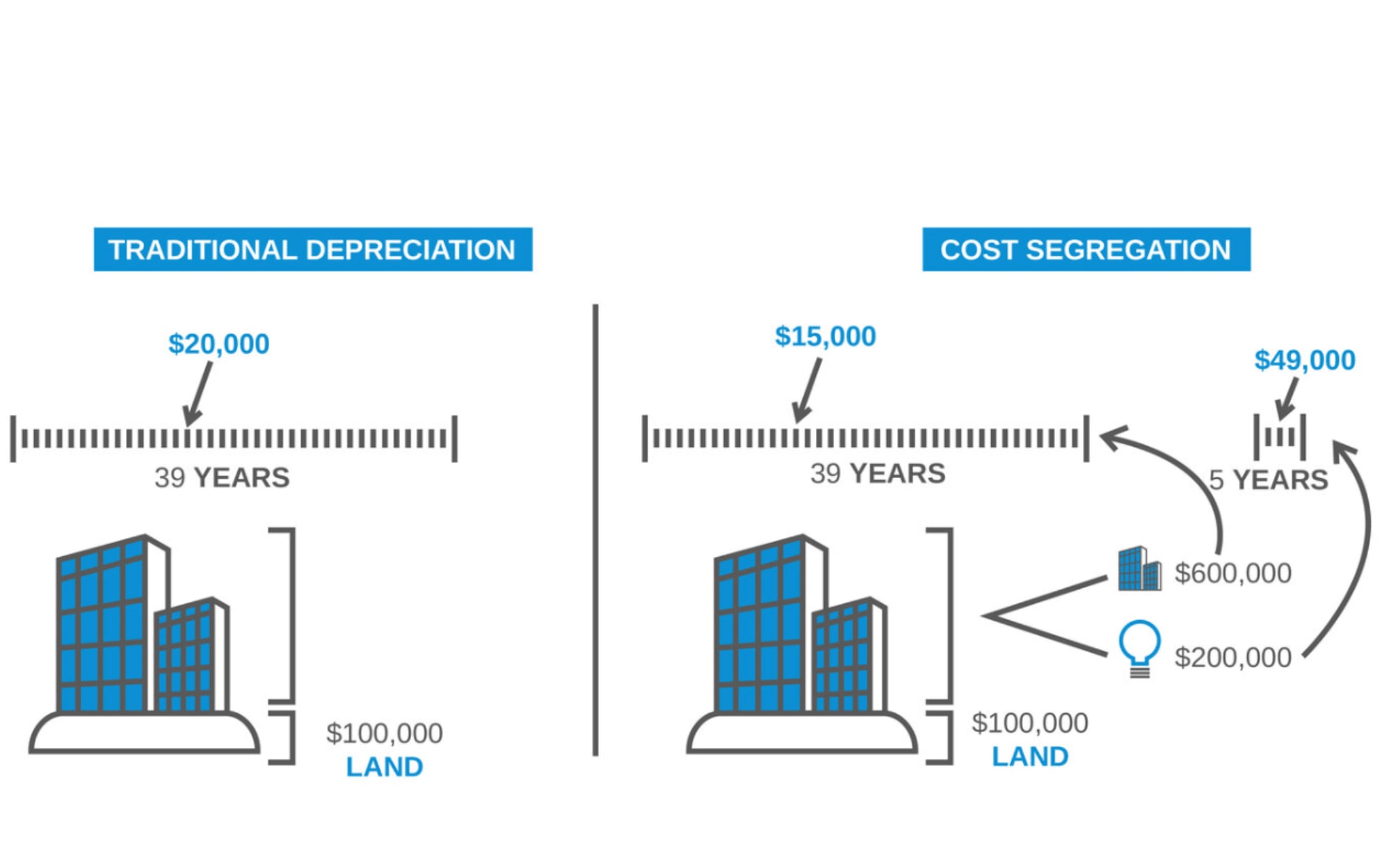

One of these strategies is a Cost Segregation Study to determine the amount of accelerated depreciation on an investment property. This strategy allows property owners to increase cash flow by “accelerating” depreciation deductions and deferring federal and state income taxes. Every time you buy an investment property, you’re entitled to full depreciation on your property.

The way a Cost Segregation study is conducted is similar to an appraisal and starts by having an engineering (or other qualified) firm take a look at the subject property and break that property down into four parts.

- The land

- Land improvement

- The building itself

- The equipment and fixtures

The last two of these parts, the building & the equipment/fixtures, are closely examined to assess the depreciation of their intrinsic value over the lifetime of the deal — usually somewhere between 20-30 years.

These two parts are significant and can end up being 65-85% of your total initial investment into the property. From there, one would front-load that depreciation to year one as a loss.

This means that any gains that you make year to year from the property are weighed against this loss. The taxes are offset by this loss, and you don’t have to pay taxes on that income. Some of these taxes are written off completely and some are deferred down the line.

When the property sells, your profits will likely overreach that initial loss. When that happens, that depreciation may be recaptured, and you will owe taxes on that money as standard income.

“Aw, man! How do we fix that?!” In our next blog post, we will examine another tax strategy that could help leverage your Real Estate losses against your ordinary income!

Still don’t fully understand? Consider this comparison.

You won the lottery.

Now you choose between a payment option. Do you take the money paid out over the next 30 years or do you take the lump sum immediately?

The clear choice seems to be to take the lump sum now and try to invest in ways that will make that money grow.

Why is that?

It could be because the future is never certain; or the current depreciation of a dollar’s value through inflation. Anything can happen between now and the end of those 30 years. Maybe the lottery system stops paying out. You might not even be around to enjoy the money then!

The same is true with cost segregation. Why take your depreciation over 27.5 or 39 years when you can front-end a large chunk of that depreciation in the first year?

Whether you’re looking to save some money on your income taxes for next tax season, or are simply a high earner looking to lower your taxes, consider speaking with your CPA about this strategy!